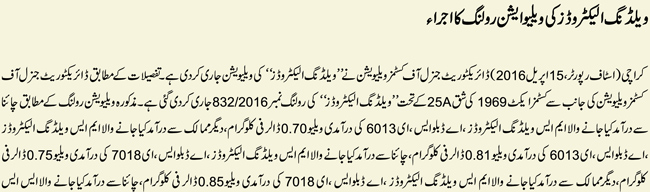

Valuation Ruling 832/2016

-

Valuation/Assessment

-

Valuation Ruling 832/2016, Against Customs Values of Welding Electrodes (MS,SS, Bronze)

Valuation Ruling 832/2016, Against Customs Values of Welding Electrodes (MS,SS, Bronze) Valuation Ruling 832

Read More »