Sunday, May 5 2024

Customkghuplay

About us

Valuation Rulings

Publication Value

Contact us

Instagram

YouTube

Twitter

Facebook

Menu

Search for

Customkghuplay

Eham Khabar

Genernal News

Anti-Smuggling

Automotive

Valuation Rulings

Publication Value

Business

FBR Transfer & Postings

International Customs Day

Mobile Phone

Port & Shipping

Videos

Home

/

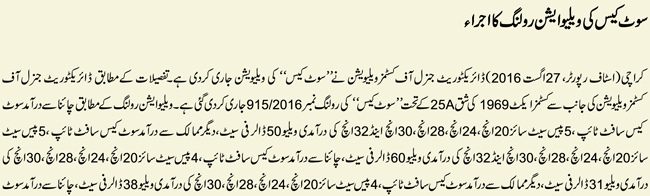

Valuation Ruling 915/2016

Valuation Ruling 915/2016

Valuation/Assessment

Valuation Ruling 915/2016, Customs Values Against Suitcases (Soft & Hard) of Low end Brand

Raza Taqvi

August 27, 2016

0

24

Read More »

Back to top button

Close

Search for